The Emerging Markets In China’s Belt & Road Initiative

Op/Ed by Chris Devonshire-Ellis

Productivity In China’s New Developing Supply Chain Still Has Some Way To Go

China’s MOFCOM and various news media outlets such as Xinhua, the People’s Daily and Global Times do their bit in both promoting the development of the Belt & Road Initiative and the impact it is having on China trade. But uncovering the actual detail is tough. Why? Because many of the Belt & Road Initiative countries – now some 152 of them – are also either significant global trading entities in their own right – think Russia – or are members of significant trade blocs, such as ASEAN, the EU, the Eurasian Economic Union, Mercasur and the Gulf Cooperation Council. This tends to obscure the actual amount of new trade development the Belt & Road Initiative is producing, as many of these include already well established trade partners. Adding them into the overall Belt & Road trade figures may make them look impressive, but it doesn’t really tell the background story of the really important issue – how much of China’s investment into the developing BRI countries is actually paying off in terms of renewed trade and investment?

Working this out requires on one hand, taking a fairly hefty pair of scissors to the Belt & Road countries China also conducts significant and well established trade with via other regional blocs. These are:

ASEAN, including Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore, Thailand & Vietnam

European Union, including Bulgaria, Croatia, Czech Republic, Estonia, Greece, Hungary, Latvia, Lithuania, Poland, Romania, Slovakia & Slovenia.

The Eurasian Economic Union, including Armenia, Belarus, Kazakhstan, Kyrgyzstan and Russia

Mercasur, which includes Argentina, Brazil, Paraguay and Uruguay

GCC, which includes Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the UAE.

However, doing so also removes legitimate BRI investments into these countries, such as Myanmar railway, Russian arctic development, EU-Eastern European infrastructure projects, and a great deal of construction activity going on in the Gulf. It also removes from the equation 37 of China’s 152 BRI nations, or just under 25%. Although stripping these nations out of any BRI trade relations isn’t an exact science, it does provide a more accurate assessment of the development trends with the remaining, or we should say, emerging, Belt & Road Initiative countries. In doing so I have taken a look at what constitutes an “emerging” belt and road nation, and stripped out those who I feel are not. It is of course subjective, and not everyone will agree with my analysis. But for discussion purposes and to gain some insight into the real picture of the emerging Belt & Road Initiative, these are the decisions I have made and the countries that feature

European Union: I have stripped out all EU countries with the exception of Greece, as it has been receiving funding from China and is a major gateway into Europe through the Chinese owned Piraeus port.

ASEAN: All countries have been stripped out except the emerging nations of Cambodia, Laos, Myanmar & Vietnam, who were the last four countries to enter into full ASEAN FTA compliance.

Eurasian Economic Union: All countries are included with the exception of Russia, which is a major trading power in its own right and inclusion would distort the emerging market figures.

Africa: All countries with a Belt & Road MoU are included

Central & South America: All countries with a Belt & Road MoU are included. Brazil is a major trading power and is excluded.

Gulf Cooperation Council: Oman is included as it is the smallest of the Oil producing nations, is diversifying away from this industry and is a gateway on the BRI to the Middle East.

Others: I have omitted all Belt & Road smaller economies such as the Caribbean and Pacific Islands etc.

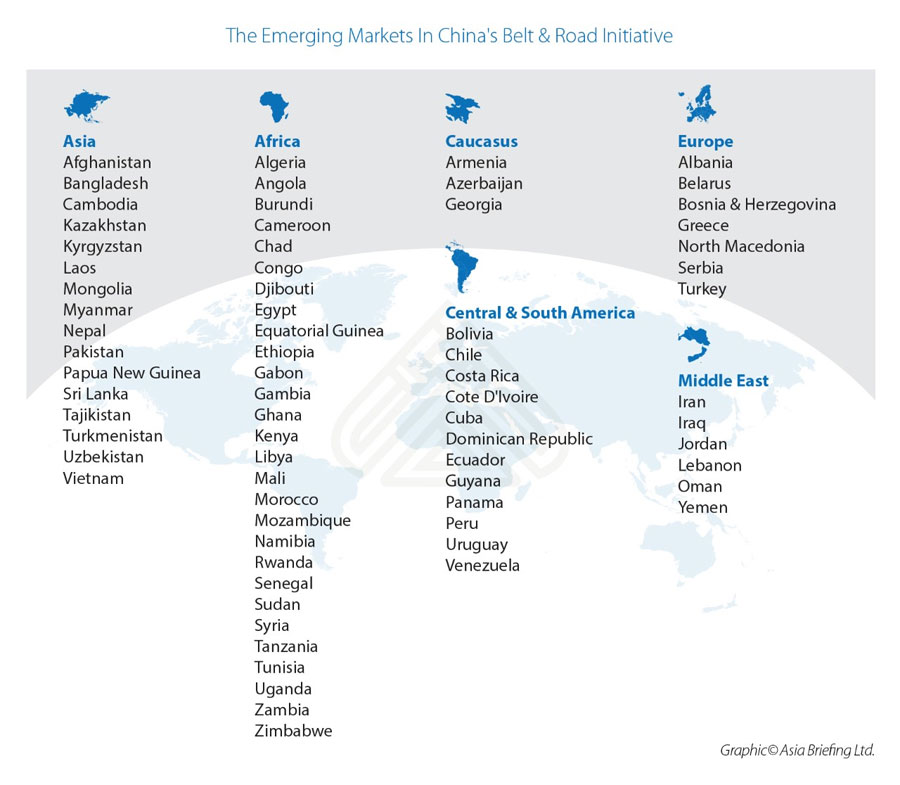

The remaining countries, what I refer to as the Emerging Markets Within The Belt & Road Initiative, produce a contents table as follows:

To get a handle on how effective China’s Belt & Road Initiative has been then on an emerging market basis, we can now look at the performance of these countries and evaluate the impact of Chinese trade and investment in this sector alone.

Here are a few takeaways, statistics courtesy of Trading Economics

Europe

The Greek economy is currently growing at 1.3% per annum, with Albania at 0.56%, North Macedonia at 4.1%, Turkey at 1.3% , Bosnia & Herzegovina at 0.6%, Serbia at 0.3% and Belarus to the east at 1.3%

Caucasus

Armenia grew by 6.5%, Azerbaijan at 3% and Georgia at 4.9%

South East Asia

The ASEAN nations: Cambodia grew at 7.5%, Laos at 6.5%, Myanmar at 6.8% and Vietnam at 6.7%. Elsewhere, Sri Lanka grew by 3.7%, and Pakistan at 5.2%.

Central Asia

The EAEU member states: Kazakhstan grew by 4.1%, & Kyrgyzstan at 5.3%. Other central Asian states: Tajikistan at 7.5%, Turkmenistan at 6.2% and Uzbekistan at 5.8%

Africa

Algeria grew at 1.5%, Cameroon at 4.2%, Chad at 1.5%, Egypt at 5.7%, Ethiopia at 9.2%, Gambia at 5.2%, Ghana at 1.6%, Kenya at 1.7%, Morocco at 2.8%, Namibia at 0.6%, Senegal at 1.2%, Tanzania at 6.6%, Uganda at 0.3% and Zimbabwe at 4%

Middle East

Iran grew at 1.8%, Jordan at 2% and The Lebanon at 1%

Central America

Costa Rica grew at 1.8%, Guyana at 4.1% and Panama at 3.1%

South America

Chile grew at 0.8%, Peru at 1% and Uruguay at 0%.

What Do The Belt & Road Emerging Markets Tell Us?

It’s a mixed bag, although mainly positive. Consistent and high levels of GDP growth are being produced in Central and South-East Asia, meaning that China’s trade relations and investments into ASEAN and the Eurasian Economic Union are paying off. Should China add product categories to the FTA it signed off last year with the EAEU then these figures will immediately further – and significantly increase.

The Caucasus remains in limbo with the EU, while China has been busy, albeit mindful of the various regional tensions, in investing in infrastructure throughout the region, using it as a southern transshipment route to the EU. That appears to be paying off. Over to Europe though, and its a different story. Economies are sluggish and much investment work still needs to be done to properly connect eastern and southern Europe to China’s Belt & Road. The EU remains impartial to China trade – they have not concluded a proposed Free Trade Agreement with China first tabled several years ago, and Brussels remains suspicious of Beijing. They’ve missed a trick – the ASEAN bloc is about to take over from the EU as China’s largest trade partner, and its exports to China are rising while the EU’s product exports to China remain sluggish in terms of export growth.

Africa is a huge continent so it is to be expected it yields mixed results, although for the most part they are sluggish to positive. However, the current GDP growth figures do not take into account the recent African Continental Free Trade Agreement, which reduced tariffs on 90% of all intra-Africa trade. When the significance of this kicks into the trade sphere we are likely to see a marked improvement.

The Middle-East emerging markets are recovering from war and sanctions, it will be some time before the infrastructure build that is being put in place will reap trade rewards. Central and South America are also mired in economic stagnation, although there are some bright spots. China is also making investments, again it will be some time before these pay off in terms of trade growth.

I roughly estimate the Emerging Belt & Road Initiative market to be worth about US$500billion in bilateral trade at present, with about US$350 billion being Chinese exports, and about US$150 billion in imports from these countries. That is against China’s customs recent announcement that the entire Belt & Road Initiative nations are currently conducting trade volumes of about US$1.4 trillion with China and exporting about US$650 billion worth of goods and services to China. As mentioned, that larger figure includes trade with larger countries that have historical trade ties with China or are part of a trade bloc that does. Once discounted, as I have done to concentrate on the Emerging Belt & Road nations, the trade figure reduces. I also estimate that the growth in trade from Emerging Belt & Road Countries is currently running at about 3% per annum. However I would expect this to increase as infrastructure projects currently under progress are completed and begin to add trade enhancement and connectivity value.

It will be interesting to see how these figures change year on year. China at present is able to cherry-pick the neighboring economies of ASEAN, while now seeing healthy opportunities elsewhere in Central and South-East Asia. Africa will almost certainly pick up trade volumes due to the recent AfCFTA deal, while the Belt & Road Europe, Middle East and Central & South America remain “under development” – emerging markets within an emerging market. We will review these statistics on a 6 monthly basis.

Related Reading

- China’s Moves Into Europe As Belt & Road Initiative Migrates West

- China’s African Moves Through The Belt & Road, Double Tax Treaties & AfCFTA

- Chinese Businesses Investing More In ASEAN. So Should Foreign Investors As Trade War Bites

About Us

Silk Road Briefing is produced by Dezan Shira & Associates. The firm provides business intelligence, legal advisory, tax advisory and on-going legal, financial and business operational support to investors throughout China, India, ASEAN and Russia, and has 28 offices throughout the region. We also provide advice for Belt & Road project facilitation. To contact us please email silkroad@dezshira.com or visit us at www.dezshira.com